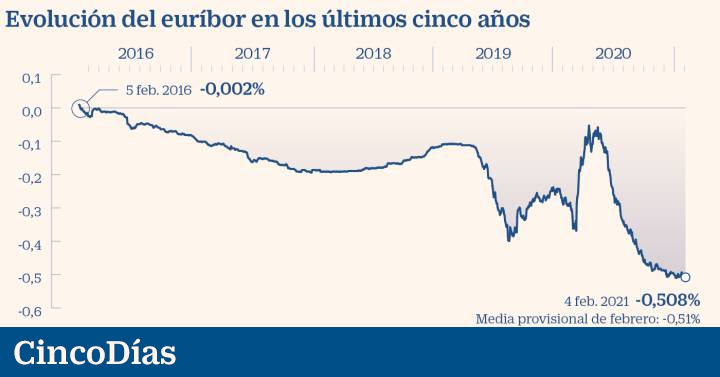

It was also Friday, February 5, 2016. Just five years ago, the

12-month Euribor

, which is used to calculate the bulk of variable mortgages in Spain, went negative for the first time in its history.

It marked -0.002% and closed the month at -0.008%.

He surprised locals and strangers in a movement that was to anticipate another unprecedented event: the reduction of interest rates by the European Central Bank (

ECB

) to the all-time low of 0% just a month later.

The Euribor has not returned to positive rates since then and the governing rates have not moved.

The evolution of the mortgage index has practically paralleled the ECB's economic stimulus measures, aimed above all at promoting financing for families and businesses and reviving inflation, and its downward trajectory has led it to record historical lows almost daily until

currently

anchor

at -0.5% levels

, something that has also amazed analysts.

During this five-year period, the Euribor has clearly benefited

holders of variable-rate mortgages

, who have seen their loans become cheaper, except for occasional rallies.

Meanwhile, the

banking system

has been the most affected, with its net interest margin significantly reduced.

The solution of the sector was to rescue and make fixed mortgages more attractive, as well as to link more to the client to scratch profitability.

They are the face and the cross of the negative Euribor during the last five years.

"The downward trend of the Euribor reflects the lax equilibrium of

the interbank market

after several years of negative interest rates and broad monetary expansion packages in the euro area," says

Olivia Álvarez, analyst at Monex Europe

.

"In view of the numerous challenges posed by the health situation and the economic crisis, it will be years before the Euribor rate returns to operating positively," he stresses.

Pandemic

Only the outbreak of the

coronavirus

last year, which unleashed uncertainty and tension in the interbank market, suddenly changed the trend of the Euribor for a few months.

The index went from around -0.3% in mid-March to 0.05% in May.

The mortgages under review became more expensive in that period.

But again, the action of the ECB in June, which irrigated the financial system with liquidity to support the economy due to the impact of Covid-19, returned the indicator to the lane of declines.

Unbridled falls that have placed the Euribor even below the -0.5% barrier set by the ECB's deposit rate, which is the interest charged by the institution to banks for parking their liquidity reserves.

"The beginning of the pandemic forced the European institution to re-relax its monetary policy in the face of the economic downturn produced by the continuous restrictions to stop the spread of the virus. The Euribor reached its peak in 2016 during the month of May, already However, in June, the ECB decided to increase the asset purchase program and this decision generated a turning point in the Euribor, which has accumulated eight consecutive months of falls ", summarizes

Joaquín Robles, from XTB

, who points out that now" European banks have a quantity of credit that is much higher than the demand, which has caused a drop in interest rates. "

The great unknown is whether the Euribor has already found its ground.

Experts argue that the index will stabilize around -0.5% and will not drop much more, but at the beginning of the year it has dropped to -0.515%.

The ECB recently suggested that it could cut interest rates and deposit rates further.

For now, the monthly average for February stands at another record low, -0.51%, 0.502 points lower than five years ago.

"During 2021 the Euribor will remain negative and in the first semester we expect it to trade in the range between -0.45% and -0.54%. We understand that it will be difficult for it to fall more than 0.5%," says Robles.

For his part,

Enrique Lluva, from Imantia

, points out that "the market thinks today that it will remain negative until December 2026", although the expert believes that the change to positive will come a little earlier.

Mortgaged

Citizens with variable mortgages have benefited from substantial savings over the years.

Taking as a reference a mortgage of 250,000 euros for 30 years with a differential of 0.99% over Euribor, the total saving from amounts to approximately 492 euros, according to iAhorro calculations.

In addition, those with spreads lower than 0.5% have stopped paying interest to the bank.

José Manuel Amor, managing partner of the Economic and Market Analysis area of Analistas Financieros Internacionales (Afi)

highlights that "the beneficiaries are all those with loans referenced to the Euribor, not just families."

In his opinion, in the absence of interest rate movements and the banking risk premium, the Euribor will be stable in the next 12-24 months. "

Banking sector

On their side, financial institutions have seen their profitability collapsed.

"Profitability is one of the main variables that characterize the financial situation of banks and the first line of defense against adverse shocks," according to the Bank of Spain, which indicates that, currently, Spanish banks are at the bottom of Europe with a profitability below zero, affected by the impact of Covid-19.

From without

commissions.org they

maintain that "probably all the damage that could be inflicted on the bank has already been inflicted, since it has had time, since February 2016, to adapt its way of working to the new reality. There has been (and will be ) massive layoffs and office closures that lower the expense account of the entities, have launched the collection of commissions and have also generated new avenues of income ".

For José Manuel Amor, "the interest margins, which is what feeds the upper part of the bank's income statement, will continue to be under great pressure and how the bank wants to transmit the fall of the Euribor will depend on the policy of each bank ".

For now, some are already charging even for deposits.

"The banks' strategy will continue to be to bet on the fixed rate, which for some time has become their best ally in trying to weather the situation of instability in the mortgage market and, specifically, at such a volatile index as is the Euribor ", they point from

iAhorro

.

The bank offers are becoming more aggressive and some fixed rates, such as those marketed by MyInvestor and Openbank, are even below 1.5%.

About half of the mortgage loans are already constituted at a fixed rate.

In this context, the comparator's director of mortgages, Simone Colombelli, assures that "we are facing a great opportunity to contract a fixed mortgage to ensure a fee with unusually low interest forever. Although, on the other hand

,

variable mortgages would be a An interesting product for a profile that does not have much aversion to risk and that wants to repay its loan in a period of 10 or 15 years at most ".

/cloudfront-eu-central-1.images.arcpublishing.com/prisa/YO5DZ3LUPREZFJDBI72KRYBPOY.jpg)

/cloudfront-eu-central-1.images.arcpublishing.com/prisa/JOPWYYFNQ5C4FB73EEEL4PBO3U.jpg)